📅 ITR Filing Deadline: July 31, 2026 for FY 2025-26 (AY 2026-27). Only 75 days remaining. Secure your CA slot →

NRI ITR-2 Filing Guide 2026 — Complete Step-by-Step for FY 2025-26

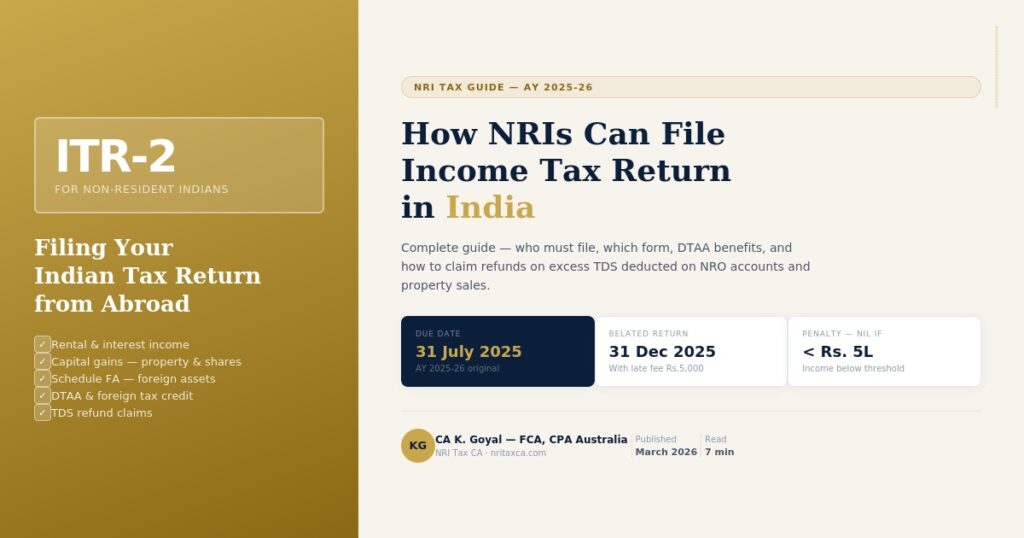

If you are a Non-Resident Indian (NRI) with income from India — rental income, interest on NRO accounts, capital gains from property or shares, or any other Indian source — you are required to file an Income Tax Return in India for FY 2025-26 (Assessment Year 2026-27). The deadline is July 31, 2026.

This guide covers everything you need to know — which ITR form to use, what income to declare, how to claim DTAA benefits, and how to avoid the most common mistakes NRIs make when filing.

Who Must File ITR as an NRI in 2026?

As an NRI, you must file an Indian Income Tax Return if any of the following apply:

- Your total income from Indian sources exceeds ₹2.5 lakh (old regime) or ₹4 lakh (new regime) in FY 2025-26

- You have capital gains from sale of property or shares in India — regardless of amount

- TDS has been deducted on your Indian income and you want to claim a refund

- You have income from a business or profession in India

- You hold foreign assets or have signing authority on foreign accounts (Schedule FA disclosure)

- You want to carry forward capital losses to offset against future gains

Even if your Indian income is below the exemption limit, filing an ITR is the only way to claim a refund of TDS that has been deducted at source — for example, 30% TDS on NRO account interest.

Which ITR Form Do NRIs Use?

| ITR Form | When to Use | NRI Applicable? |

|---|---|---|

| ITR-1 (Sahaj) | Salary + one house property + other income | NO — NRIs cannot use ITR-1 |

| ITR-2 | Salary, house property, capital gains, foreign income/assets | YES — Most NRIs use this |

| ITR-3 | Business or professional income in India | YES — if NRI has Indian business income |

| ITR-4 (Sugam) | Presumptive income from business | NO — NRIs cannot use ITR-4 |

The answer for most NRIs is ITR-2. Use ITR-3 only if you run a business or practice in India. Never use ITR-1 or ITR-4 as an NRI — your return will be defective.

What Income Do NRIs Declare in ITR-2?

Taxable Indian Income for NRIs

| Income Type | Taxability | TDS Rate |

|---|---|---|

| NRO account interest | Fully taxable at slab rates | 30% + surcharge + cess |

| NRE account interest | Fully EXEMPT | No TDS |

| FCNR account interest | Fully EXEMPT | No TDS |

| Rental income from Indian property | Taxable after 30% standard deduction | 30% by tenant (Section 195) |

| Long term capital gains — property | 12.5% (post July 2024 purchases, no indexation) | 12.5% on sale value |

| Short term capital gains — property | Taxable at slab rates | 30% on sale value |

| Long term capital gains — listed shares | 12.5% above ₹1.25 lakh | Broker deducts |

| Short term capital gains — listed shares | 20% (STT paid transactions) | Broker deducts |

| Dividends from Indian companies | Taxable at slab rates | 20% TDS |

| Foreign salary / income | NOT taxable in India for NRIs | No TDS |

How to Determine Your Residential Status for FY 2025-26

Your residential status determines what income is taxable in India. An individual is treated as an NRI for FY 2025-26 if they spent fewer than 182 days in India during the financial year (April 1, 2025 to March 31, 2026).

There is an important exception: Indian citizens whose total Indian income (excluding foreign income) exceeds ₹15 lakh are treated as “deemed residents” even if they spent fewer than 182 days in India — provided they are not taxable in any other country. This primarily affects people living in zero-tax countries like UAE.

Three Residential Categories

| Status | Condition | What is taxable in India |

|---|---|---|

| NRI | Less than 182 days in India | Only Indian-source income |

| RNOR | Transitioning from NRI to resident | Indian income + certain foreign income |

| Resident (ROR) | 182+ days in India | Global income — including foreign salary |

Important: Count your days carefully using passport stamps and airline records. Even a small error can change your tax status and significantly increase your tax liability.

Step-by-Step — How to File ITR-2 as an NRI for FY 2025-26

Step 1 — Gather All Required Documents

- PAN card

- Aadhaar number (must be linked to PAN)

- Form 26AS / AIS / TIS from the Income Tax portal — shows all TDS deducted against your PAN

- Bank statements for all NRO accounts

- Form 16A from banks (TDS certificate for NRO interest)

- Rental income details — rent receipts, municipal tax paid

- Sale deed and purchase deed if property was sold during the year

- Broker contract notes for share transactions

- Tax Residency Certificate (TRC) from your country of residence — for DTAA claims

- Form 10F — filed electronically on the Income Tax portal

Step 2 — Download and Reconcile Form 26AS

Log into the Income Tax portal at incometax.gov.in → My Account → Form 26AS. This document shows every TDS deduction against your PAN. Your ITR must match Form 26AS exactly — any mismatch triggers a notice.

Also check AIS (Annual Information Statement) which shows all financial transactions reported against your PAN including property purchases, large bank credits, and share transactions.

Step 3 — Choose Between Old and New Tax Regime

| Feature | Old Regime | New Regime (Default) |

|---|---|---|

| Basic exemption | ₹2.5 lakh | ₹4 lakh |

| Section 80C deductions | Available (up to ₹1.5 lakh) | Not available |

| Home loan interest (Section 24) | Available | Limited |

| Tax rates | Higher slabs | Lower slabs |

| Best for NRIs when | High deductions available | Simple income, few deductions |

Note for NRIs: The tax rebate under Section 87A is NOT available to NRIs. Only resident individuals can claim this rebate. This is one of the most common errors in NRI returns.

Step 4 — Claim DTAA Benefits (Critical Step)

If your country of residence has a Double Taxation Avoidance Agreement (DTAA) with India, you may be entitled to a lower TDS rate or a foreign tax credit. To claim DTAA benefits you must:

- Obtain a Tax Residency Certificate (TRC) from your country’s tax authority

- File Form 10F electronically on the Income Tax portal

- Submit both documents to the payer (bank, tenant, company) before income is paid

- Declare DTAA benefit in Schedule TR of your ITR-2

DTAA benefit by country for NRO interest:

| Country | Standard TDS | DTAA Rate on Interest | Saving |

|---|---|---|---|

| 🇦🇪 UAE | 30% | 12.5% | 17.5% saving |

| 🇺🇸 USA | 30% | 15% | 15% saving |

| 🇬🇧 UK | 30% | 15% | 15% saving |

| 🇦🇺 Australia | 30% | 15% | 15% saving |

| 🇨🇦 Canada | 30% | 15% | 15% saving |

| 🇸🇬 Singapore | 30% | 15% | 15% saving |

Step 5 — Fill Schedule FA (Foreign Assets Disclosure)

NRIs filing ITR-2 whose total Indian assets exceed ₹1 crore must disclose foreign assets in Schedule FA. This includes:

- Foreign bank accounts

- Foreign property and real estate

- Foreign equity and debt interests

- Foreign trusts and beneficiary interests

- Any other foreign financial interest

Penalty for non-disclosure: ₹10 lakh per year under the Black Money Act. This is one of the most serious compliance requirements for NRIs.

Step 6 — File ITR-2 on the Income Tax Portal

- Log in to incometax.gov.in

- Go to e-File → Income Tax Returns → File Income Tax Return

- Select Assessment Year 2026-27

- Select ITR-2

- Choose filing mode — online (recommended) or offline (download utility)

- Fill in all schedules — Schedule HP (house property), Schedule CG (capital gains), Schedule OS (other sources), Schedule TR (DTAA relief), Schedule FA (foreign assets)

- Compute tax and verify the amount matches your expectation

- Submit and e-verify within 30 days

Step 7 — E-Verify the Return

Filing the ITR is not complete until you e-verify it. An unverified ITR is treated as if it was never filed. E-verification options:

- Aadhaar OTP (fastest — instant verification)

- Net banking (login to your bank → e-verify)

- Bank account EVC (electronic verification code)

- DSC (Digital Signature Certificate)

E-verify within 30 days of filing. Missing this deadline means the return is invalid and you must refile.

Key Deadlines for FY 2025-26 (AY 2026-27)

| Event | Deadline |

|---|---|

| Regular ITR filing deadline | July 31, 2026 |

| Belated ITR (with penalty) | December 31, 2026 |

| Updated ITR (ITR-U) with additional tax | Up to 2 years from end of assessment year |

| E-verification after filing | Within 30 days of filing |

Penalties for Late Filing

| Income level | Late filing penalty |

|---|---|

| Total income up to ₹5 lakh | ₹1,000 |

| Total income above ₹5 lakh | ₹5,000 |

| Interest on tax due (Section 234A) | 1% per month on tax payable |

Most Common NRI ITR-2 Mistakes

Mistake 1 — Using ITR-1 instead of ITR-2

NRIs cannot use ITR-1. If you file ITR-1 as an NRI, the return is defective and you will receive a notice. Always use ITR-2.

Mistake 2 — Not declaring NRO account interest

Many NRIs believe NRO interest is “already taxed via TDS so no need to declare.” This is wrong. You must declare the income in your ITR — TDS is just advance tax. The return is how you reconcile actual liability vs TDS paid.

Mistake 3 — Claiming Section 87A rebate

NRIs are NOT eligible for the Section 87A rebate of up to ₹12,500 (old regime) or ₹60,000 (new regime for income up to ₹12 lakh). Claiming this incorrectly will generate a demand notice.

Mistake 4 — Not filing Form 10F before DTAA claim

You cannot claim DTAA benefit in your ITR without having first filed Form 10F electronically. Retrospective filing is not accepted. File Form 10F at the start of every financial year.

Mistake 5 — Wrong residential status

Declaring yourself as “Resident” when you are an NRI means your foreign income becomes taxable in India. Always determine residential status before filing and count days precisely.

Mistake 6 — Not reconciling with Form 26AS before filing

If your declared income does not match Form 26AS, the Income Tax Department’s system automatically generates a mismatch notice. Always download and reconcile Form 26AS before filing.

Mistake 7 — Not e-verifying within 30 days

A filed but unverified ITR is treated as invalid. The deadline for e-verification is 30 days from the date of filing. Many NRIs forget this step.

Mistake 8 — Missing Schedule FA disclosure

If you have foreign assets — bank accounts, property, investments — and do not disclose them in Schedule FA, the penalty is ₹10 lakh per year under the Black Money Act.

Frequently Asked Questions — NRI ITR-2 Filing 2026

Q: I am an NRI in UAE. Is my salary taxable in India?

No. Salary earned for services performed outside India is not taxable in India for an NRI. Only income sourced from India — like NRO interest, rental income, or capital gains on Indian property — is taxable.

Q: I have only NRO account interest income of ₹1.8 lakh. Do I need to file ITR?

If your income is below ₹2.5 lakh (old regime) or ₹4 lakh (new regime), you are not required to file. However, if TDS has been deducted at 30%, filing an ITR is the only way to claim a refund — which you should.

Q: Can I file ITR-2 from outside India?

Yes. ITR-2 is filed online on the Income Tax portal from anywhere in the world. You need your PAN, Aadhaar-linked mobile for OTP verification, and internet access.

Q: What if I missed the July 31 deadline?

You can file a belated return up to December 31, 2026 with a penalty of ₹1,000 (income up to ₹5 lakh) or ₹5,000 (income above ₹5 lakh). However you lose the ability to carry forward losses.

Q: My tenant deducted 30% TDS on rent but my actual tax slab is 20%. Can I get a refund?

Yes. File ITR-2 declaring the rental income, compute actual tax at 20%, and claim the excess TDS as a refund. Refunds are typically processed within 3-6 months of filing.

Q: I sold property in India this year. Which schedule in ITR-2 do I fill?

Declare the capital gain in Schedule CG (Capital Gains). For long-term gains, show the purchase price, indexed cost (for pre-July 2024 purchases), and any Section 54 or 54EC exemptions claimed.

Q: Do I need to show my NRE account balance in ITR-2?

NRE account interest is exempt and does not need to be declared as income. However, if your total Indian assets exceed ₹1 crore, you may need to disclose the account in Schedule FA.

Q: What documents does my CA need to file my ITR-2?

Form 26AS / AIS, bank statements for NRO accounts, Form 16A from banks, rental income details, property sale documents (if applicable), share transaction contract notes, TRC and Form 10F for DTAA claims, and passport copy for residential status verification.

Q: Can I revise my ITR-2 after filing if I made a mistake?

Yes. A revised return can be filed up to December 31, 2026 for FY 2025-26. There is no penalty for filing a revised return before this deadline.

Q: Is it compulsory to link Aadhaar with PAN for NRI ITR filing?

PAN-Aadhaar linking is mandatory for resident Indians. NRIs who do not have an Aadhaar number may request exemption by updating their NRI status on the Income Tax portal.

NRI ITR-2 Filing — What We Handle

Our team handles complete ITR-2 filing for NRIs — residential status determination, income computation, DTAA analysis, Schedule FA disclosure, Form 10F filing, and e-verification. Every return is reviewed by an ICAI-registered Fellow Chartered Accountant.

- ✓ All NRI income types — NRO interest, rental income, capital gains, dividends

- ✓ DTAA benefit claims for USA, UK, UAE, Australia, Canada, Singapore

- ✓ Foreign tax credit computation

- ✓ Schedule FA disclosure for foreign assets

- ✓ Complete reconciliation with Form 26AS / AIS before filing

- ✓ E-filing and e-verification included

- ✓ Written confirmation of every step

| Service | Price |

|---|---|

| NRI ITR-2 — Basic (interest + rental income) | Starting ₹3,499 |

| NRI ITR-2 — With capital gains | Starting ₹4,999 |

| NRI ITR-2 — With property sale + repatriation | Starting ₹6,999 |

| Form 145 + 146 + ITR-2 complete package | Starting ₹6,999 |

ITR deadline: July 31, 2026 — 75 days remaining

Email us at hello@nritaxca.com — fixed quote within 2 hours.

Start Your ITR Filing →

This guide is updated as of April 2026 and reflects provisions of the Income Tax Act 2025 applicable for FY 2025-26 (AY 2026-27). Consult a qualified Chartered Accountant for advice specific to your situation.

Focus keyphrase: NRI income tax return India

Before filing ITR-2, use our free NRI tax calculator to estimate your tax liability, TDS credit and refund amount. Our CA team can file your ITR-2 — get started here.

Before filing ITR-2, use our free NRI tax calculator to estimate your tax liability, TDS credit and refund amount. Our CA team can file your ITR-2 — get started here.

Use our free NRI Tax Calculator to instantly estimate your property TDS, refund amount and ITR obligation → Calculate Now